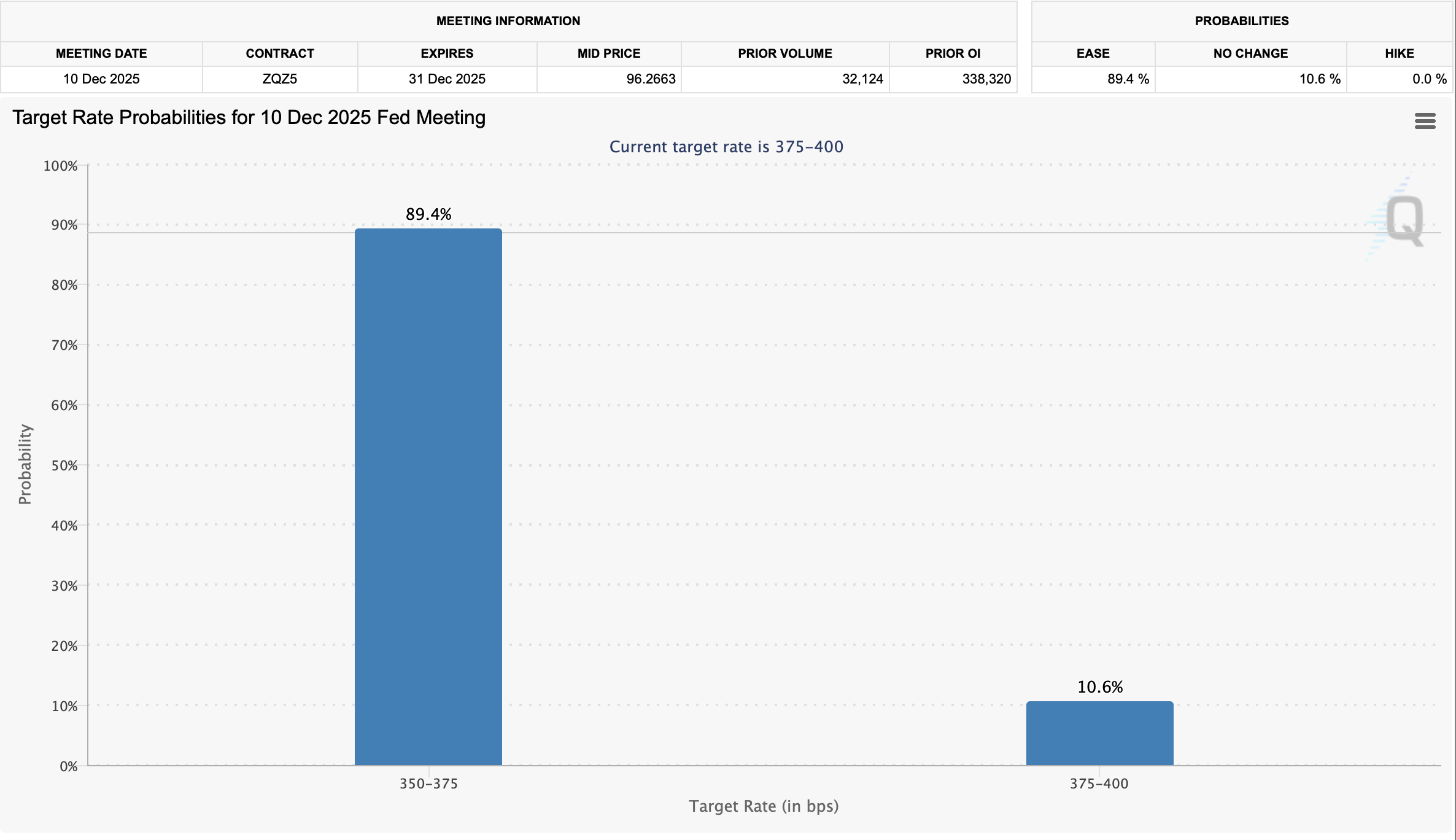

Expectations for a December rate cut are now overwhelming. New CME FedWatch data shows markets pricing an 89.4% probability that the Federal Reserve will lower its target range to 3.50%–3.75% at the December 10 meeting.

Only 10.6% of traders expect no change, and 0% foresee a hike. The shift underscores a market that sees the Fed as out of runway and ready to act.

This aligns with the updated projections from Standard Chartered and Citigroup, both of which now anticipate a 25 bps cut this week. The current effective rate sits at 3.89%, above the official 3.50%–3.75% range, reinforcing the sense that policy is already too tight for weakening conditions.

Why December Looks Locked In

Standard Chartered describes the move as an “insurance cut.” With the labor market softening and government shutdown delays leaving policymakers short on fresh data, a preemptive adjustment is seen as the least risky path. The bank argues that a small cut now provides stability without forcing the Fed into a larger rescue later.

Citigroup shares the view. Rising unemployment and a clear tonal shift from several Fed officials point toward a dovish pivot. Citi analysts say the December meeting is the moment the Fed signals it is ready to adapt to an economy drifting away from the tight-growth narrative of early 2025.

The futures market agrees. The FedWatch bar chart shows traders overwhelmingly concentrated in the lower-rate bucket, making December one of the most consensus-driven meetings in years.

Where the Forecasts Split: The 2026 Path

The picture becomes far less unified once the calendar turns.

Standard Chartered sees the December move as a potential one-off. Its base case holds that rates could remain unchanged through most of 2026 unless conditions deteriorate faster than expected. Even so, the bank’s latest communication hints at an early-2026 cut, possibly in January, before stepping back again.

Citigroup takes a much more active stance. Their team expects a series of 25 bps cuts across the first half of 2026, pushing the policy rate into a 3.00%–3.25% range. That would create a gradual easing cycle rather than a single pivot point.

This divergence reflects uncertainty around the incoming Fed leadership expected in spring 2026. A new chair could lean more dovish or more conservative, depending on the administration’s priorities and inflation trends.

What the Market Will Watch Next

The Fed’s December decision may be largely priced in, but the follow-through will hinge on real-time data:

- Labor market softness will dictate whether a single cut is enough.

- Inflation readings will shape the pace of any 2026 moves.

- Fed leadership changes could redefine the tone of policy entirely.

For now, Wall Street is aligned on one key point: the cut this week is almost certain. Whether that marks the start of a cycle, or simply a strategic adjustment, remains the question that will drive markets into the new year.