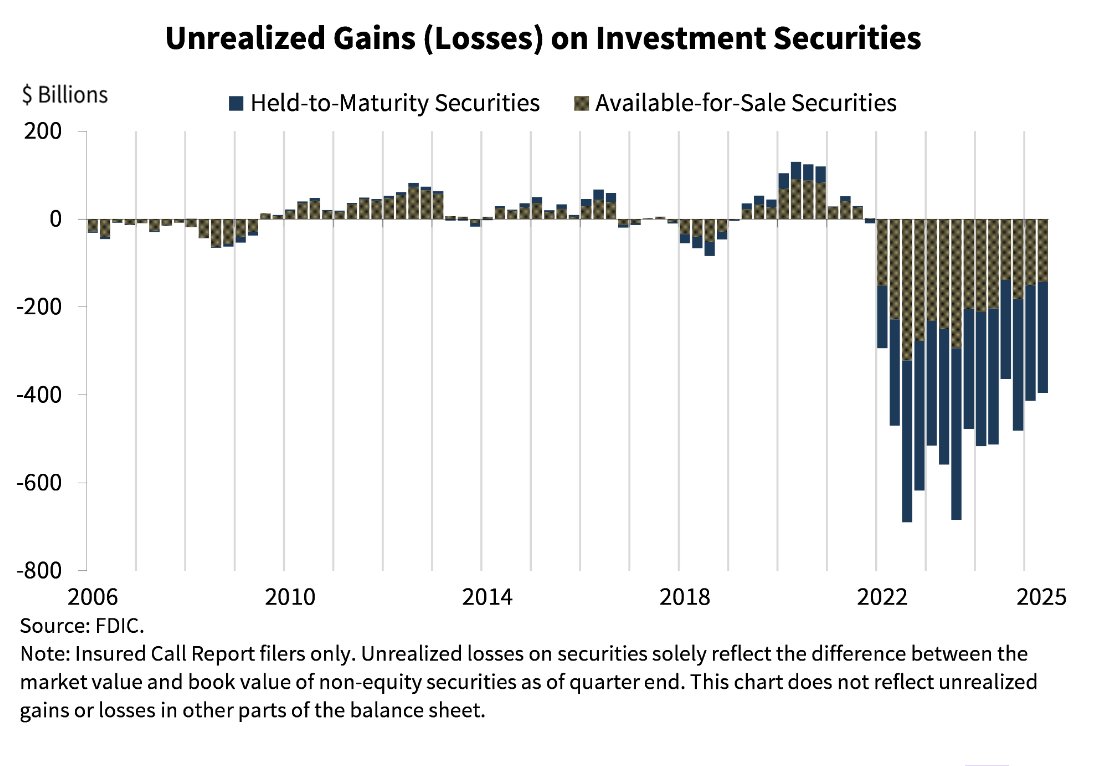

New figures from the Federal Deposit Insurance Corporation (FDIC) reveal that US banks are carrying $395 billion in unrealized losses on their investment securities portfolios for Q2, one of the largest loss positions on record and a stark reminder of the financial stress still lingering across the banking sector.

The chart, which breaks losses into held-to-maturity (HTM) and available-for-sale (AFS) securities, shows that the pressure on bank balance sheets remains deep and prolonged. Most of the unrealized losses stem from fixed-income securities purchased during the zero-rate era. As interest rates surged, those securities lost a significant portion of their market value.

A Loss Profile Worse Than 2008

The FDIC’s historical series highlights something striking: the scale of unrealized losses since 2022 surpasses the drawdowns seen during the 2008 financial crisis. While banks are not required to mark HTM securities to market on income statements, the losses still weigh on regulatory capital flexibility and limit the ability to sell these assets without crystallizing damage.

AFS securities, represented in blue on the chart, show even steeper declines, as these must be marked at fair value each quarter. Many institutions have already taken substantial hits through their equity accounts as a result.

Why the Losses Matter

Unrealized losses may not immediately signal insolvency, but they reduce balance-sheet strength in several key ways:

- They restrict liquidity, because banks are discouraged from selling underwater assets.

- They tighten lending conditions, as capital buffers become more fragile.

- They elevate systemic risk, particularly if deposit conditions deteriorate or if rapid outflows force asset liquidation.

This same pressure contributed to last year’s banking turmoil, when Silicon Valley Bank and others were unable to cover fast-moving withdrawals while sitting on deep bond losses.

The Policy Context

The persistently depressed value of bank securities comes as high interest rates continue to reshape the US financial landscape. Even if rate cuts begin in 2026, the road back to par could take years, especially for long-dated bonds purchased at extremely low yields.

Regulators are monitoring the sector closely. The FDIC has warned throughout 2024 and 2025 that unrealized losses remain a key vulnerability, particularly for regional banks that rely heavily on securities portfolios rather than diversified income streams.

Outlook

As of Q2, the FDIC’s data suggests that the US banking system has not fully recovered from the rapid rate shock of the past three years. With nearly $400 billion in embedded losses, any renewed stress, whether from deposit flight, economic slowdown, or credit deterioration, could again expose the system’s weak points.

For now, the losses remain on paper. But the longer interest rates stay elevated, the harder it becomes for banks to escape them without significant restructuring or additional capital.