Fresh analysis shared by The Kobeissi Letter highlights a striking historical pattern: when the CBOE Volatility Index (VIX) spikes above key thresholds, the S&P 500 has repeatedly delivered strong 12-month forward returns.

The data, compiled from market performance between 1991 and 2022, suggests that periods of heightened volatility have often created major buying opportunities rather than long-term market stress.

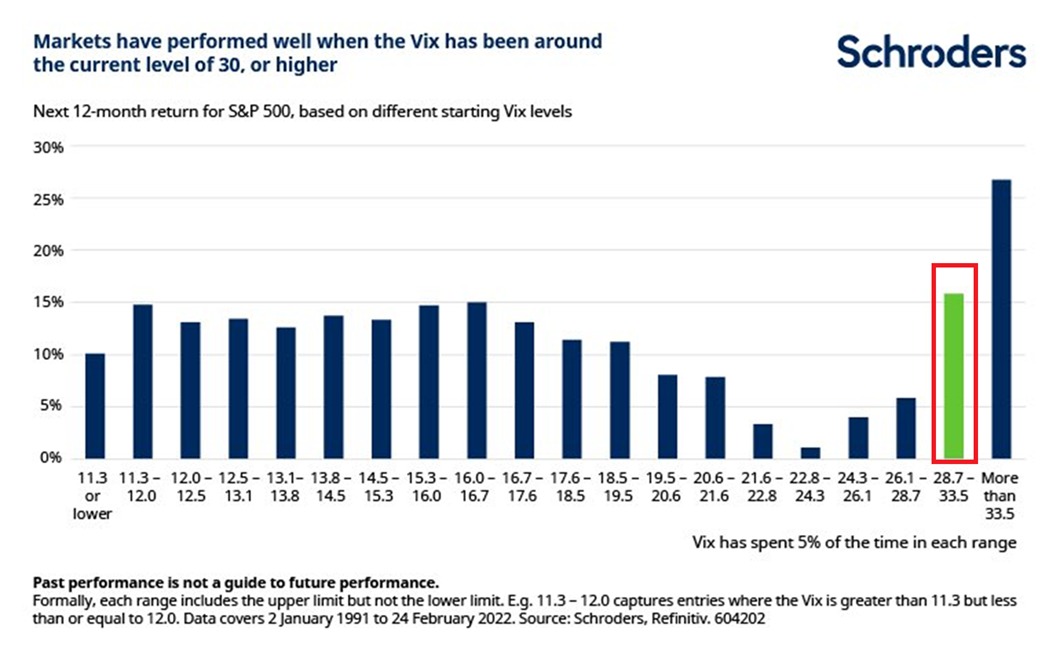

High VIX Readings Often Mark Market Bottoms

According to the research, when the VIX jumps above 28.7, the S&P 500 has historically returned an average of +16% over the following year. When volatility crosses 33.5, average forward returns improve even further to +27%, making elevated VIX conditions one of the strongest statistical indicators of future upside.

These results contrast sharply with calmer market periods. When the VIX trades between 11.3 and 12.0, the S&P 500’s average 12-month return is only +15%, lower than the returns generated after high-stress spikes.

The dataset covers more than three decades, including recession periods, credit stresses, and geopolitical volatility, yet the relationship remains consistent.

Why This Pattern Matters

Historically, market volatility tends to cluster around periods of fear-driven selling, forced deleveraging, or macro uncertainty. These conditions frequently push equity valuations sharply lower in a short time. As selling pressure exhausts itself, markets often stabilize and generate strong forward performance as capital re-enters risk assets.

The latest Schroders chart included in the research reinforces this pattern: forward returns increase noticeably when starting from VIX levels in the upper 20s and 30s, with the strongest returns recorded when volatility exceeds 33.5.

What It Suggests About Current Conditions

With the VIX recently moving sharply higher amid global market stress, this historical backdrop provides an important context. Elevated volatility has rarely been a terminal risk indicator for equities. Instead, it has more often signaled the late stages of a fear-driven sell-off and the early stages of a recovery.

While past performance does not guarantee future results, over 30 years of data suggest that periods of extreme VIX readings have consistently presented long-term buying opportunities for equity investors.