The venture capital playbook that once dominated crypto is showing visible cracks.

According to The DeFi Edge, 85% of tokens launched in 2025 are now trading below their initial listing price. Many VC-backed projects are barely breaking even, while some sit deep in negative territory. The data signals a sharp shift in how the market is valuing early-stage crypto deals.

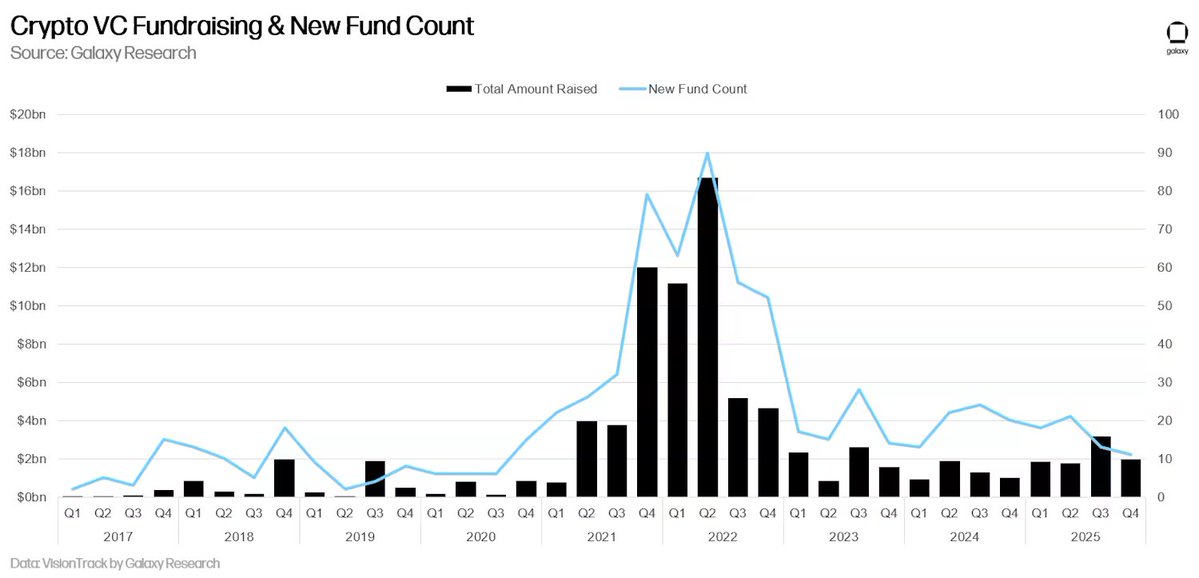

The 2022 Boom vs. Today’s Reality

In Q2 2022, crypto venture capital hit peak euphoria. Funds raised nearly $17 billion in a single quarter, with more than 80 new funds launched. Limited partners were aggressively allocating capital to anything branded “crypto.”

That environment no longer exists.

Since 2022:

- VC returns have steadily declined

- The number of new funds has dropped to a five-year low

- Last quarter’s fundraising totaled just 12% of Q2 2022 levels

While VCs deployed $8.5 billion last quarter, up 84% quarter-over-quarter, most of that capital originated from funds raised during the 2022 cycle. It is not fresh money entering the ecosystem.

In fact, total capital deployed between 2023 and 2025 roughly matches what was raised in 2022 alone.

The End of the “Top VC” Premium

There was a time when having a top-tier venture firm on a project’s cap table was viewed as a major catalyst. That signal effect has weakened significantly.

With 85% of new token launches underwater, the traditional model, raise a large private round, launch a token, distribute liquidity, and rely on market momentum, is losing effectiveness. Retail participants have become more selective, and liquidity is thinner than during the 2021–2022 cycle.

The strategy of launching tokens primarily to provide exit liquidity for early investors appears far less viable under current conditions.

What Comes Next

There is a structural shift underway.

As venture influence fades, the projects most likely to succeed are those with:

- Active users

- Sustainable revenue

- Clear product-market fit

The decline in easy venture funding could result in fewer opportunistic launches and fewer chains competing for speculative capital. Instead, builders may increasingly focus on long-term product development rather than short-term token events.

If this trend continues, the market may gradually transition from capital-driven hype cycles toward fundamentals-driven growth.